|

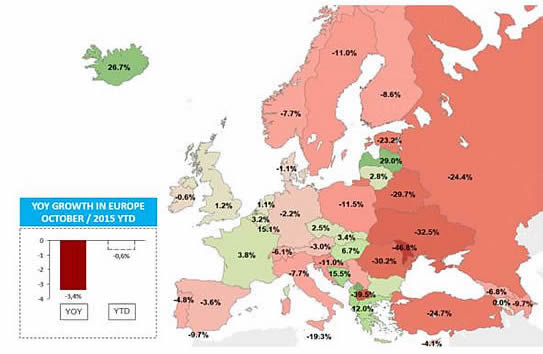

There were 67,209 business aviation departures in Europe in October

2015 according to WINGX`s latest monthly Business Aviation Monitor - a 3.4% decline year on year.

Flight hours fell 5%, with a 6% decline in Private

activity and a 4% fall in AOC activity.

The declines this month came in Southern Europe mainly, with sizeable decreases in Italy and Spain. Central European activity was weak, with fewer flights from Germany, Austria, and

Switzerland. There were also some heavy declines across Scandinavia.

Flight activity in Europe´s leading market, France, was robustly up this month, mainly due to domestic trips and Prop activity. Activity in the UK also increased

YOY. Smaller countries

with growth in October included Belgium, Netherlands, and Greece.

Year on year trend in flight

activity

Overall, Western Europe sustained its slight last 12 month recovery. But flights connecting Europe with other global regions mostly fell: transatlantic flights slightly down; CIS region and

Africa significantly reduced.

Aircraft

Business jet flights,

representing 59% of all business aviation activity in October, declined most at -5% YOY, of which Private jet flights declined

7% and heavy jet sectors fell by 10%. Heavy jet AOC sectors were down almost 20% this month.

The largest YOY deficits in business jet activity came in Switzerland and Italy. Relatively large declines

were also evident in Sweden, down 18% YOY. Russian and Turkish jet sectors dropped >25% YOY. Private jet flights from Europe to the CIS region have fallen a third YTD.

Light and Entry Level jets posted some gains this month. VLJ Charter activity was well up. Turboprop activity declined

however, eroding the recent strong recovery in Prop activity. PC12 flights declined, but King Air 200 activity was up.

Airports

The top airports saw substantial declines this month, with more than 10% dips in Private activity at the busiest, although AOC flights were up at Luton and Le Bourget. Business jet flights

increased at Farnborough, Stuttgart, Biggin Hill and Oxford.

Richard Koe, Managing Director of WINGX Advance, comments:

“The trend in business aviation activity has disappointed since the end of the summer, with October showing increased

weakness in South as well as East Europe. Central Europe is essentially flat, and only in France and UK have there been signs of continuing recovery, mainly in the Charter market.

Across the market, the main burden right now is the fast-falling demand for heavy and midsize jets. But underlying the overall stagnation in activity this year, there has been some broad

recovery in light jet and turboprop activity, as well as more specific boosts to activity through individual platforms such as the Global Express and Challenger 300.”

| click

on the icon to access the

current WINGX Business Aviation

Monitor |

|

WINGX

Advance is a data research and consulting

company based in Hamburg, Germany. WINGX

analysis provides actionable market intelligence

for the business aviation industry. WINGX

services include: Market Intelligence Briefings,

Customised Research, Strategic Consulting,

Market Surveys. WINGX customers range from

aircraft operators, OEMs, airlines, maintenance

providers, airports, fixed base operators, fuel

providers, regulators, legal advisors, leasing

companies, banks, investors and private jet

users. |