|

|||

|

|||

|

Bombardier has announced the pause of its Learjet 85 program. The pause is due to weak demand for the aircraft and follows a downward revision of the company's business aircraft market forecast. This reflects the continued weakness of the Light aircraft category since the economic downturn. As a result, the Company will record a pre-tax special charge in the fourth quarter of 2014 of approximately $1.4bn mainly related to the impairment of the Learjet 85 development costs. Additionally, Bombardier will reduce its workforce by approximately 1,000 employees at its sites in Querétaro, Mexico, and Wichita, United States. A severance provision of approximately $25m will be recorded as a special item during the first quarter of 2015. “Bombardier constantly monitors its product strategy and development priorities,” said Pierre Beaudoin, President and Chief Executive Officer, Bombardier Inc. “Given the weakness of the market, we made the difficult decision to pause the Learjet 85 program at this time. We will focus our resources on our two other clean-sheet aircraft programs under development, CSeries and Global 7000/8000, for which we see tremendous market potential. Both programs are progressing well.”

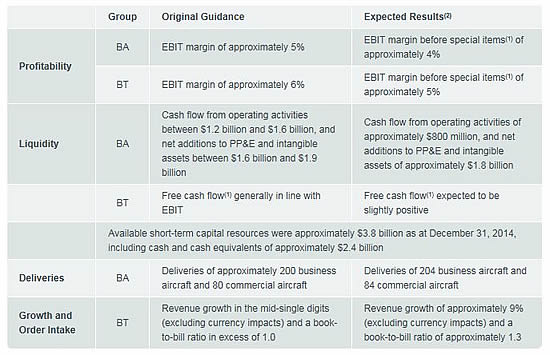

Bombardier’s Wichita and Querétaro sites remain critical facilities in key markets. Wichita is a multifaceted facility and is the location of final assembly activities for the Learjet 70 and Learjet 75 aircraft, the Bombardier Flight Test Center as well as a Service Center. In addition to contributing to many of Bombardier’s aircraft programs, the Querétaro site recently completed its Global 7000/8000 aft fuselage manufacturing building. Furthermore, following a review of preliminary results compiled by Bombardier for the fiscal year ended December 31, 2014, it has become clear that certain financial guidance previously provided will not be met. Based on these preliminary results, Bombardier is updating its guidance for 2014. Summary guidance for 2014 Earnings before financing expenses, financing income and income taxes (EBIT) before special items(1) at Aerospace (BA) is expected to be approximately 4% compared with a previous guidance of 5%. The variation is mainly due to increased provisions for credit and residual value guarantees, pricing pressure on new aircraft sold, as well as a decrease in fair value of used aircraft. EBIT before special items(1) at Transportation (BT) is expected to be approximately 5% compared to a previous guidance of 6%. This variation is mainly due to revised escalation assumptions for some contracts which impacted estimated future revenues.

Cash flow from operating activities at Aerospace is expected to be approximately $800m while net additions to property, plant and equipment (PP&E) and intangible assets are expected to be approximately $1.8bn, compared with a previous guidance for cash flow from operating activities between $1.2bn and $1.6bn and net additions to PP&E and intangible assets between $1.6bn and $1.9bn. The variation in Aerospace’s cash flow from operating activities is mainly due to a lower level of customer advances, a lower EBIT and an increase in used aircraft inventory. Free cash flow(1) for Transportation is expected to be slightly positive compared with a previous guidance of free cash flow generally in line with EBIT. This variation is mainly due to a different cash flow profile in some contracts and a lower level of advances on options in relation to framework contract agreements. As of December 31, 2014, available short-term capital resources were approximately $3.8bn, including cash and cash equivalents of approximately $2.4bn. Aerospace exceeded its delivery targets with a total of approximately 290 aircraft (204 business, 84 commercial and two amphibious aircraft), compared with a guidance of 200 business and 80 commercial aircraft deliveries. This represents a 22% increase compared with the deliveries of 238 aircraft for the previous year (180 business, 55 commercial and three amphibious aircraft). Transportation revenues (excluding currency impacts) are expected to increase by approximately 9% in 2014, compared with a guidance of revenue growth in the mid-single digits, with a book-to-bill ratio of approximately 1.3 compared with a guidance in excess of 1.0. |

|||

| BlueSky Business Aviation News | 22nd January 2015 | Issue #304 | |||

| BlueSky - your weekly business and executive aviation news - every Thursday | |||